Income-oriented investors tend to like midstream master limited partnerships (MLPs) for their high yields and increasing distributions. However, it isn’t often that an MLP raises its distribution by 50% or more.

That’s just what Western Midstream (NYSE: WES) did last month when it took its quarterly distribution from $0.575 per unit to $0.875. That’s a 52% increase. It is also important to point out that this is its base distribution and not a special or variable dividend. The stock now yields an attractive 9.4% using its closing price on May 13.

Let’s take a look at the pipeline operator’s first-quarter results and where its distribution could be headed in the future.

A great start to the year

Western Midstream started the year in great fashion, recording record Q1 adjusted EBITDA of $609 million. That was a 22% year-over-year increase. Free cash flow came in at $225 million, a nearly 60% year-over-year jump.

It saw record natural gas throughput across its asset base, with volumes up 2% from the previous quarter. Operated crude and NGL (natural gas liquid) volumes also rose 2% from the previous quarter.

The company’s operations in the Delaware Basin in west Texas and southeastern New Mexico — the most prolific oil basin in the U.S. — saw solid natural gas volume increases of 3% quarter over quarter.

Meanwhile, the company’s operations in the DJ Basin, primarily in northeastern Colorado, continue to recover. Natural gas volumes rose 2% sequentially in the basin, while crude and NGL volumes jumped 7%.

The company sees these strong throughput trends continuing through the rest of the year for all three products it transports. As a result, it is now projecting that adjusted EBITDA and cash flow will be at the high end of its prior guidance. Western Midstream had previously forecast full-year adjusted EBITDA to be between $2.2 billion and $2.4 billion and for free cash flow to come in between $1.05 billion and $1.25 billion.

In addition to its strong Q1 results, Western Midstream also closed the sale of five non-core assets, collecting about $790 million in proceeds. It took some of that cash and bought back about $150 million in debt.

Where the distribution is headed

Based on the $0.575 distribution Western Midstream paid in February, it paid out $223 million in cash distributions in the quarter. That total will go up to about $340 million this quarter based on its increased distribution, and it will pay out about $1 billion in distributions for the remaining three quarters in the year. Based on its guidance, it should generate about $1.7 billion in operating cash flow the next three quarters.

It plans to spend about $95 million in maintenance capital expenditures (capex) over the rest of the year, so its distributable cash flow (DCF) will be about $1.6 billion. DCF is operating cash flow minus maintenance capex. That gives it a solid distribution coverage the rest of the year.

Depending on how much it spends in growth capex, it should generate between $350 million and $500 million in excess cash flow after distributions over the rest of the year.

Without reducing debt any further, the company is on track to get to 3 times leverage (net debt/adjusted EBITDA) by year end. At that point, Western Midstream will have reached its leverage goal and be set up to pay out enhanced distributions above its base distribution in 2025.

If it can generate $500 million in excess cash flow after its base distributions next year, the company could pay out another $0.25 or more a quarter in enhanced distributions. Of course the amount will be impacted by how much growth capex it will spend, along with opportunities to repurchase stock and/or pay down more debt.

A 9.4% yield with the opportunity of enhanced distributions next year makes Western Midstream a very attractive stock for investors looking for income.

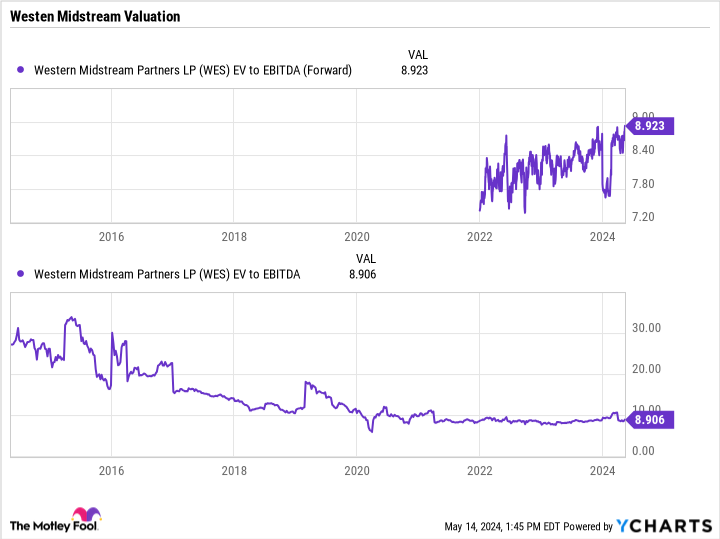

A great value

Despite recent solid gains in the stock, Western Midstream still trades at an attractive enterprise value (EV)-to-adjusted EBITDA multiple of just under 9. This is one of the most common metrics to value midstream companies, as enterprise value takes into account net debt, while EBITDA removes non-cash expenses.

On its earnings call, management argued that not only is Western Midstream undervalued, but that the entire midstream space is. The company said that under the old MLP model, the average valuation of midstream stocks was 13.7 on an EV/EBITDA basis, while today it is around only 8.

That is despite the industry being in a much stronger position with better balance sheets, good liquidity, and strong free-cash-flow generation, compared to a decade ago when midstream MLPs had negative free cash flow and leverage was increasing.

This is something I firmly believe. Midstream companies are in much better shape today than previously, but trade at a pretty big discount. While this valuation gap will not close overnight, it is a long-term opportunity for investors. Western Midstream, meanwhile, is one of the most attractive stocks in the midstream space given its yield, balance sheet, and growth prospects.

Should you invest $1,000 in Western Midstream Partners right now?

Before you buy stock in Western Midstream Partners, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Western Midstream Partners wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $566,624!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Geoffrey Seiler has positions in Western Midstream Partners. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Western Midstream Just Raised Its Distribution by 52%. Where Is the Dividend Heading for This 9.4%-Yielding Stock? was originally published by The Motley Fool

Signup bonus from