This has been a terrible year for Snowflake (NYSE: SNOW) shareholders. Though the data cloud provider started 2024 on a positive note, the stock is now down 48% from the 52-week high it hit in mid-February thanks to issues ranging from management turnover to increasing competition to quarterly results that haven’t met expectations.

However, that sharp pullback may have created an opportunity for savvy investors, especially considering the valuation at which Snowflake is trading right now.

Snowflake’s growth is likely to accelerate

When Snowflake released the results for its fiscal 2025 first quarter (ended April 30) in May, it reported that product revenue had increased 34% year over year to $790 million. That was significantly higher than its guidance range of $745 million to $750 million. Additionally, the company raised its full-year product revenue guidance to $3.30 billion from the prior outlook of $3.25 billion.

The revised figure points toward a 24% increase in revenue from fiscal 2024. However, there is a good chance Snowflake will raise its revenue guidance further as the year progresses considering the impressive growth in its remaining performance obligation (RPO) last quarter. RPO refers to the “amount of contracted future revenue that has not yet been recognized.”

This metric includes Snowflake’s deferred revenues — funds the company has received in advance for services that will be delivered later — and non-cancellable contracts that will be “invoiced and recognized as revenue in future periods.” The fact this metric grew at a much faster pace than Snowflake’s top line suggests the company’s revenue growth is likely to accelerate.

More importantly, Snowflake is forecasting an incredible expansion in its total addressable market thanks to the emergence of artificial intelligence (AI). In its 2024 Investor Day presentation, Snowflake management asserted that its total addressable market could jump from $152 billion in 2023 to $342 billion in 2028. And the company has a series of products lined up to capitalize on the AI-driven opportunity within the data cloud market.

A lot of those products are set to be made generally available to customers in the current fiscal year. These include the likes of Cortex AI, Document AI, and Snowflake Copilot. Cortex AI, for instance, will enable Snowflake customers to build generative AI applications such as chatbots with the help of large language models (LLMs), using their proprietary data.

Meanwhile, Snowflake Copilot has been designed to help the company’s customers assist in writing structured query language (SQL) code and help improve productivity. And Document AI is a proprietary LLM that customers can use to extract data from different types of documents. As Snowflake introduces these products widely, it may be able to increase spending from its existing customers while also attracting new ones.

It is worth noting that Snowflake exited its fiscal Q1 with 9,822 customers, an increase of 21% from the prior-year period. However, the number of customers that are contributing more than $1 million in product revenue annually to Snowflake increased 30% year over year to 485. The company may be able to sustain this trend of increased spending from customers thanks to new growth drivers such as AI, as well as its focus on launching new products.

However, Snowflake’s detractors may argue its growth is coming at the expense of its margins. After all, the company’s non-GAAP product gross margin fell slightly in the previous quarter to 76.9%. The company has also reduced its full-year margin guidance to 75% from the previous estimate of 76%.

Not surprisingly, analysts are forecasting Snowflake’s adjusted earnings to drop to $0.62 per share in fiscal 2025, down from $0.98 per share last year. While that’s a big drop, they should bounce back next fiscal year to $0.99 per share. Management attributed the hit to profitability to “increased GPU-related costs related to our AI initiatives.”

But at the same time, these investments are set to unlock a robust long-term growth opportunity for Snowflake and should ideally allow the company to earn more revenue from its existing customers as they buy into its AI-related offerings. Any short-term pain could eventually pave the way for a stronger bottom-line performance in the long run, which is why investors should focus on the big picture here.

The valuation makes the stock an attractive bet right now

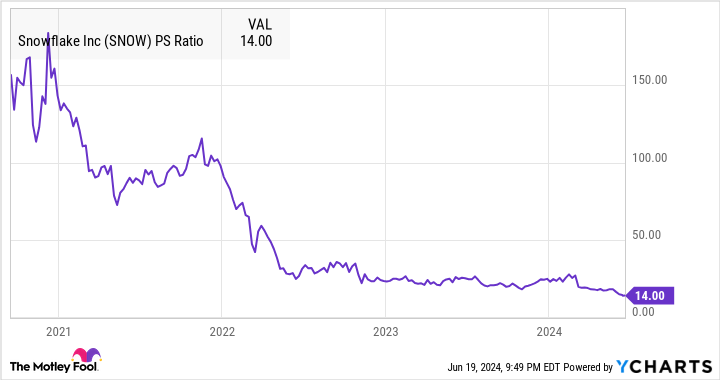

Investors can buy Snowflake stock at a relatively attractive price-to-sales ratio of 14, which is well below its multiple of 25 at the end of 2023. Of course, Snowflake’s sales multiple remains higher than the U.S. tech sector’s average of 8. However, Snowflake is now cheaper by that metric than it has ever been.

Given Snowflake’s solid revenue pipeline and better-than-expected revenue growth, savvy investors may want to consider buying the stock right now. After all, 71% of the 48 analysts covering Snowflake rate it as a buy, and their median 12-month price target for the stock is $200 — 60% above the current price.

If Snowflake’s top-line growth continues to outpace expectations, the stock could soar again.

Should you invest $1,000 in Snowflake right now?

Before you buy stock in Snowflake, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Snowflake wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $723,729!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 24, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Snowflake. The Motley Fool has a disclosure policy.

1 Magnificent Artificial Intelligence (AI) Growth Stock Down 48% to Buy Hand Over Fist Before It Starts Soaring was originally published by The Motley Fool

Signup bonus from