Social Security is a vital income source for many of its roughly 53.5 million recipients. For retirees who have spent years working and paying taxes into the program, it’s a well-earned financial safety net.

Regardless of when you plan to retire or the role Social Security will play in your retirement finances, having an idea of what monthly benefit to expect is essential for financial planning.

According to the latest data from the Social Security Administration, the average monthly benefit for someone claiming at age 62 is $1,275. If you look at averages by gender, there’s a disparity because of the difference in average lifetime earnings. The average benefit for men is $1,421, while it’s $1,141 for women.

While any income in retirement is helpful, the hard truth is the average monthly benefit at that age won’t be enough to cover living expenses for many retirees.

How your benefits are affected by claiming at age 62

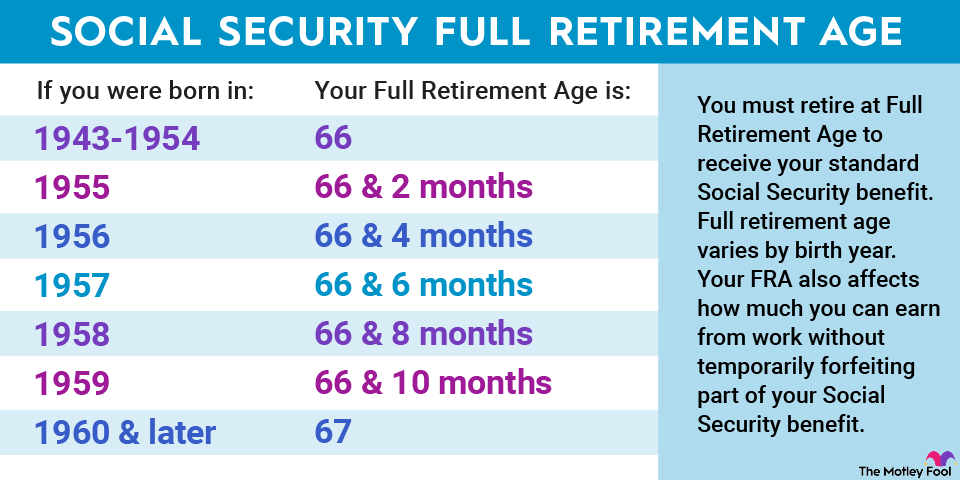

Your full retirement age (FRA) is one of the most important numbers you should know about Social Security and retirement in general. It’s the age when you’re eligible to receive your primary insurance amount (PIA), which you can think of as your standard benefit. From there, monthly benefits are either decreased or increased based on when you claim relative to your FRA.

The earliest you can claim Social Security benefits is 62. In general, claiming benefits before your FRA reduces them by 5/9 of 1% each month within 36 months of FRA. Beyond 36 months, Social Security further reduces benefits by 5/12 of 1% each month.

For someone whose FRA is 67, claiming benefits at 62 will reduce their monthly payout by 30%. For example, if you were due to receive $2,000 at your FRA of 67, claiming at 62 would bring it down to $1,400.

Using the 80% rule to put your monthly benefit into perspective

There’s no one-size-fits-all approach regarding how much you’ll need in retirement. Different plans, locations, and lifestyles will all require different amounts of savings. However, there are rules of thumb you can use to help guide you.

One of them is the 80% rule, which says you should aim to generate 80% of your last working year’s income annually in retirement. If we’re following that guidance, here are examples of how much someone should aim to have in annual retirement income:

|

Last Working Year’s Income |

Annual Income Goal in Retirement |

|---|---|

|

$40,000 |

$32,000 |

|

$60,000 |

$48,000 |

|

$80,000 |

$64,000 |

|

$100,000 |

$80,000 |

Calculations by author.

An average Social Security benefit of $1,275 amounts to $15,300 annually. If we’re going by the 80% rule, this amount would only work for those whose income in their last working year was $19,125.

For a lot of people, that amount alone won’t get the job done. It helps if you’re living in a house that’s paid off or don’t have a car payment, but many retirees aren’t quite that fortunate. With rising prices and increased healthcare costs, meeting your financial needs with Social Security benefits alone is challenging, even with regular cost-of-living adjustments.

A reminder of the importance of having multiple sources of retirement income

The 80% rule is just one example of high-level guidance. If you plan to downsize your lifestyle in retirement, you’ll be able to lower the percentage. If you plan to upgrade your lifestyle, you should probably stick with 80% or increase it slightly.

In either case, the more significant point is how important it is to strive for multiple sources of retirement income. A 401(k) might not be available to you because it depends on your employer, but a retirement account like an IRA can be a great option as well.

You can open an IRA on your own, similar to a bank account, and it often provides great tax breaks, offers flexibility in investment choices, and has early-withdrawal exceptions that can come in handy for life events like purchasing your first home or paying for higher education.

You can also lean on investments from a brokerage account. History has shown that dollar-cost averaging over time, regardless of how small the investments are, can really add up to significant amounts. You won’t get IRA-like tax breaks in a brokerage account, but it can still be a great place to park your savings.

There’s no such thing as being overprepared for retirement, but you can absolutely be underprepared. As valuable as Social Security may be to retirees, it shouldn’t be their only source of income.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets” ›

The Motley Fool has a disclosure policy.

Here’s the Average Social Security Benefit at Age 62 — and Why It’s Not the Best News for Retirees was originally published by The Motley Fool

Signup bonus from