Undervalued stocks are rare gems in today’s stock market. They can be hard to find, but they can be lucrative for investors who look for the right features. Workday (NASDAQ: WDAY) is one of the more impressive companies available on the market today, and the stock’s valuation should have more investors thinking about buying shares.

Workday is a powerhouse in its industry

Workday has over 20% market share of the human capital management (HCM) industry — or human resources. This places the cloud software business alongside giants like ADP (NASDAQ: ADP) and Oracle (NYSE: ORCL). Gartner has named the company a leader in enterprise resource planning cloud software for eight consecutive years. The company’s cloud-based HCM software is among the most respected and most popular available, with more than 10,000 customers — including 60% of the Fortune 500.

Workday boasts data to back up those leadership claims. The company reports gross revenue retention of around 95%. This means that it lost only 5% of the revenue from customers that were on its books one year ago. This is also before factoring in expansions or upsells on existing customer accounts, which would offset at least a portion of the lost 5%. Gross dollar retention of 95% is a bullish metric for software-as-a-service (SaaS) businesses.

Workday also achieved a 13% return on invested capital (ROIC). ROIC is an efficiency ratio that measures a company’s profits relative to its financial resources. High ROIC indicates efficient operations, and Workday’s performance is impressive, given its focus on growth rather than profit maximization.

The company could likely improve its profit margins by cutting back on hires and investments in technology necessary to fuel future growth, which would drive ROIC even higher. However, Workday maintains a balanced approach that delivers impressive expansion alongside cash-flow generation.

High retention and ROIC indicate product quality and pricing power. That’s evidence of a wide economic moat. Economic moats are sustainable competitive advantages, which are attractive features to investors. Workday’s wide moat is attributable to product quality and switching costs, which make it difficult for current and future rivals to poach its customers.

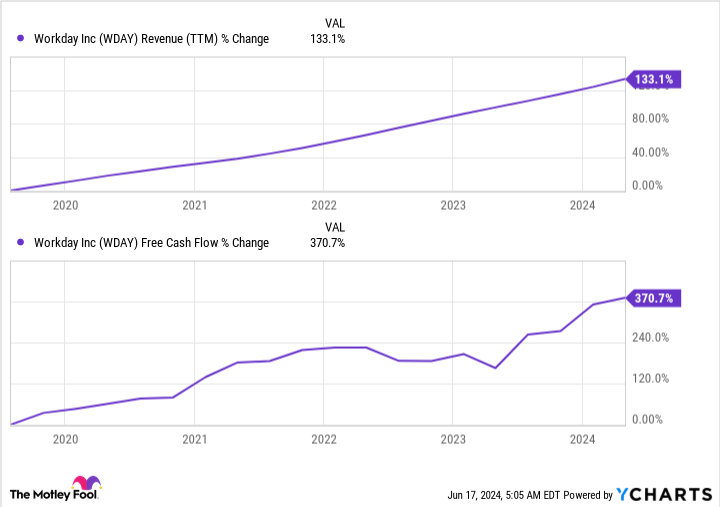

Financial results have been impressive

Workday has nailed the headline financial results in addition to those efficiency metrics. The company grew its sales 18% in its most recent quarter, surpassing Wall Street’s forecasts. The HCM leader also beat analyst estimates for earnings, with adjusted EPS of $1.74. The market reacted negatively to the company’s reduced full-year revenue guidance, but investors should find some comfort in a slight increase in its operating margin forecast.

While Workday’s sales growth rate is slowing, it’s still expanding. That adds to a history of consistent revenue increases, which has been difficult to sustain for many promising software businesses through economic turmoil. Central banks have raised interest rates around the world to combat inflation, fueling concerns about slowing growth and recession. Slowing growth rates have become fairly common, and Workday continues to build on past success.

The company’s shift toward profitability has been even more impressive. Workday reported meaningful net profits for the first time last year, and it expects earnings to expand from here. Its free cash flow has outpaced sales by a wide margin over the past five years, which is important for shareholders.

If the company is experiencing slowing growth, it’s demonstrating its ability to generate profits and tons of cash at its current scale. This gives the business concrete fundamentals to support its valuation.

Workday trades at a reasonable valuation

Workday’s forward price-to-earnings ratio is 31, and its price-to-cash-flow ratio is below 25. Those aren’t the cheapest valuation ratios you’ll see in the market, but they’re attractive when you consider the company’s growth potential. Workday expects to deliver 17% revenue growth next year, and recent results suggest that profits and cash flow will significantly outpace the top line.

Workday’s growth expectations mean that the stock could be subject to volatility thanks to changes in its outlook or capital market cycles. However, the company has the necessary ingredients for continued success along with a reasonable valuation that sets the stock up for healthy shareholder returns.

Should you invest $1,000 in Workday right now?

Before you buy stock in Workday, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Workday wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $830,777!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

Ryan Downie has positions in Automatic Data Processing. The Motley Fool has positions in and recommends Oracle and Workday. The Motley Fool recommends Gartner. The Motley Fool has a disclosure policy.

A Few Years From Now, You’ll Wish You’d Bought This Undervalued Stock was originally published by The Motley Fool

Signup bonus from