I’ll be upfront: Nvidia is the artificial intelligence (AI) king. There’s not a lot of evidence to dispute this claim if you consider its reach, business growth, and the universal nature of its graphics processing units (GPUs) that power AI.

However, if you move beyond Nvidia, there’s still another layer of successful businesses riding the same wave. One of those is Super Micro Computer (NASDAQ: SMCI). Often referred to as Supermicro, the company builds highly customizable servers that house Nvidia’s GPUs to give its clients the computing power they need to run complex models.

So, could Supermicro be the secondary king of AI? And should it be in your stock portfolio?

Strong growth, but not as much as some would like

Before the AI boom, Supermicro’s business wasn’t all that exciting. Although its servers could be tailored to running AI models, conducting drug research, or engineering calculations, that market wasn’t that large. However, once the AI arms race kicked off, Supermicro experienced rapid growth in demand for its servers dedicated to AI computing.

But not everyone is a Supermicro customer. Unlike Nvidia, whose superior products stand apart from the competition, Supermicro has multiple competitors. Hewlett-Packard and Dell are two Supermicro competitors, but their offerings aren’t as modular as Supermicro’s.

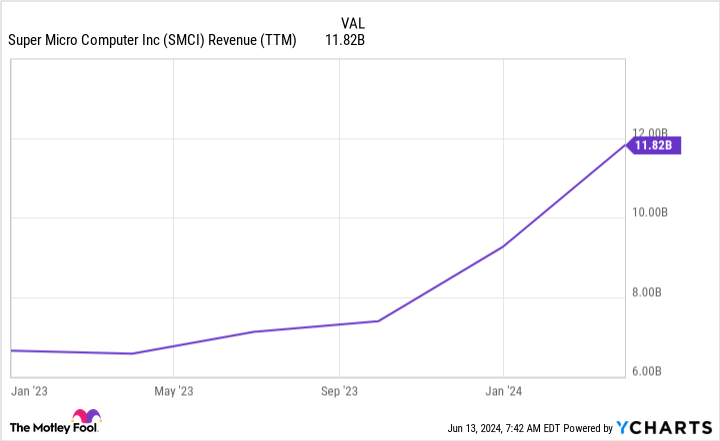

As a result, the market for Supermicro’s services is much smaller than that of Nvidia. Still, that doesn’t mean it can’t be a successful business. Revenue in the third quarter of Supermicro’s fiscal 2024 (ended March 31) rose 200% year over year to $3.85 billion.

That’s incredible growth, but investors found one metric to nitpick: quarterly growth. Revenue was only up 5% quarter over quarter, which indicates that demand isn’t rapidly expanding for Supermicro. Compared to Nvidia’s Q1 FY 2025 (ending April 28) revenue growth of 18%, Supermicro isn’t seeing similar product interest levels.

For Q4, management expects about $5.3 billion in sales, which would deliver strong quarter-over-quarter growth, but year-over-year growth would decelerate to about 143%. But this brings us to an interesting point: Supermicro’s market opportunity.

Management’s revenue goal is within reach

Also competing with Supermicro are the cloud computing providers. If a business doesn’t want to invest capital in building its own server to access the computing power needed to run AI models, it could rent that power from a cloud computing provider like Amazon Web Services or Microsoft Azure. However, this business also has a partnership aspect, as Supermicro provides some of the hardware for the big cloud computing companies.

As a result, management has been upfront with investors about what it believes its market opportunity is. Supermicro set a goal of $25 billion in revenue, and if it hits its Q4 revenue target, it will have nearly $15 billion in trailing-12-month revenue. Although management has raised its revenue goal once already (increasing it from $20 billion), if Supermicro hits its revenue goal, it will still be a very expensive stock.

Should Supermicro generate $25 billion in annual revenue combined with its Q3 profit margin of 10.5%, it would generate about $2.63 billion in profits. At Supermicro’s current market capitalization of $45 billion, that would price the stock at 17 times forward earnings.

That’s not a very expensive price, but if that’s the business’s ceiling, investors may want to pass. Individual investors aim to find strong companies that can compound for years to come. The current AI boom will likely be peak business for Supermicro, so I think investors should turn elsewhere to find other opportunities.

Thanks to AI, Supermicro will be a successful company and grow tremendously; the problem is that most of that growth is already priced in.

Should you invest $1,000 in Super Micro Computer right now?

Before you buy stock in Super Micro Computer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Super Micro Computer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $808,105!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Amazon. The Motley Fool has positions in and recommends Amazon, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Beyond Nvidia: Can Super Micro Computer Be the King of Artificial Intelligence (AI) Hardware? was originally published by The Motley Fool

Signup bonus from