Down more than 30% in 2024 alone, there’s no doubt that value investors will be starting to circle Boeing‘s (NYSE: BA) stock. Indeed, there’s a robust case for buying a company that’s part of an effective duopoly with Airbus in the global wide-body and commercial narrow-body airplane market. On balance, is the stock a buy? Here’s the lowdown.

The case for buying Boeing stock

Boeing bulls accept that the company has had quality control issues but note that Boeing’s indispensable role in the aviation industry continues. Despite delivery delays caused by the need to improve production quality in 2024, Boeing still has the potential to grow deliveries. Moreover, given the importance of volume growth on margin expansion to Boeing, hitting delivery targets can significantly increase Boeing commercial airplanes (BCA) margins and profits as it delivers on its backlog of 5,625 airplanes.

In addition, management’s free-cash-flow (FCF) target of $10 billion in 2025 to 2026 means the stock trades on just 11.1 times FCF in 2026 — a startlingly cheap valuation for a stock with such a strong market position in a growing industry.

Boeing’s labor negotiations

Unfortunately, there’s a problem with the investment thesis. As previously discussed, the $10 billion in FCF in the 2025 to 2026 target is open to question. In fact, it’s open to many questions. I want to point out three of them in more detail.

First, there’s uncertainty around the labor negotiations over a collective-bargaining agreement with the International Association of Machinists (IAM) that expires in September. As UPS investors discovered last year during their company’s negotiations with the Teamsters Union, new contracts can be costly in the current environment.

It’s no secret that the aerospace industry has been battling shortages of skilled workers after the lockdowns caused many to leave the industry and not return due to retirement or the search for alternative employment. Moreover, inflation has been relatively high over the last couple of years, which points to potentially fractious negotiations with unions reportedly asking for more than 40% pay raises.

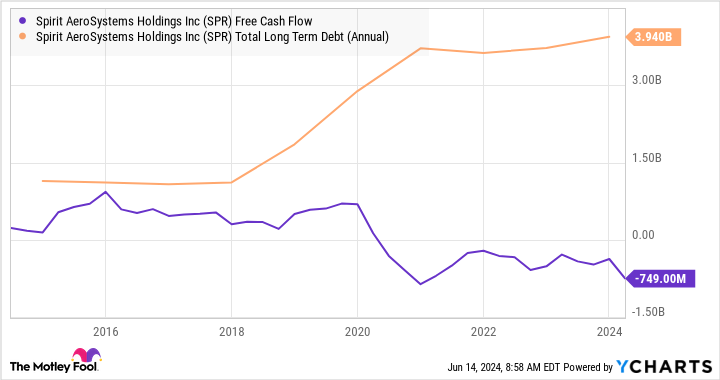

Spirit AeroSystems could be a drain on cash

Second, whether or not Boeing eventually buys key supplier Spirit AeroSystems (NYSE: SPR), Boeing might invest cash into the company. Buying Spirit, formerly part of Boeing and the provider of “the majority of the airframe content for the Boeing B737, and multiple significant structural components of the Boeing B787,” according to Spirit’s SEC filings, makes sense. Boeing needs to ensure its vital supplier can keep up with the pace of the future-volume ramp at Boeing, notably on the 737 MAX.

However, Spirit is a company that has hemorrhaged cash in recent years, while its debt load has gone the other way.

Boeing made advancements of $425 million in the spring to help the company’s near-term financial situation. That’s a sign of financial stress, and the news of Spirit’s CFO Mark Suchinski standing down in early June will only add fuel to the speculative fire.

It’s reasonable to be concerned about the potential for Spirit to be a cash drain for Boeing.

Boeing needs a new CEO

Third, it’s disappointing that the Boeing board hasn’t announced a new CEO yet. The current CEO, David Calhoun, announced in late March that he would stand down at the end of the year.

However, there’s still no news of who will replace him. This is somewhat disappointing; given that Boeing’s board contains some heavy hitters in the industry, it’s reasonable to expect that they will help ensure a smooth transition. David Gitlin (touted as a potential CEO) is the former president of UTC Aerospace Systems and the current Carrier Global CEO. Akhil Johri is the former CFO of United Technologies, and David Joyce is the former CEO of GE Aviation.

A new CEO with a new vision and a track record of ensuring manufacturing execution would significantly improve the investment case.

Is Boeing stock a buy?

It’s possible that the new CEO will remove the $10 billion in FCF in the 2025 to 2026 target as soon as possible. Wall Street doesn’t believe this will happen; the analyst consensus is for $8.2 billion in FCF in 2026, and investors shouldn’t rush to pencil it into their valuation assumptions.

Meanwhile, the labor negotiations, Spirit AeroSystems, and the lack of news on a CEO also hang over the stock, as does the ongoing struggle to ramp airplane production and return the defense business to consistent profitability. It all adds up to making Boeing a stock to avoid for now.

Should you invest $1,000 in Boeing right now?

Before you buy stock in Boeing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Boeing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $808,105!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool recommends United Parcel Service. The Motley Fool has a disclosure policy.

Boeing Stock: Buy, Sell, or Hold? was originally published by The Motley Fool

Signup bonus from