SoFi Technologies (NASDAQ: SOFI) stock has gone through some wild swings since the company went public in 2020. Investors have alternately been excited about it and concerned about where it’s going, and after the stock more than doubled in 2023, it’s down by 30% so far this year.

While there are valid reasons for the market’s misgivings, in my view, this year’s plunge has overshot the mark.

SoFi is expanding its business

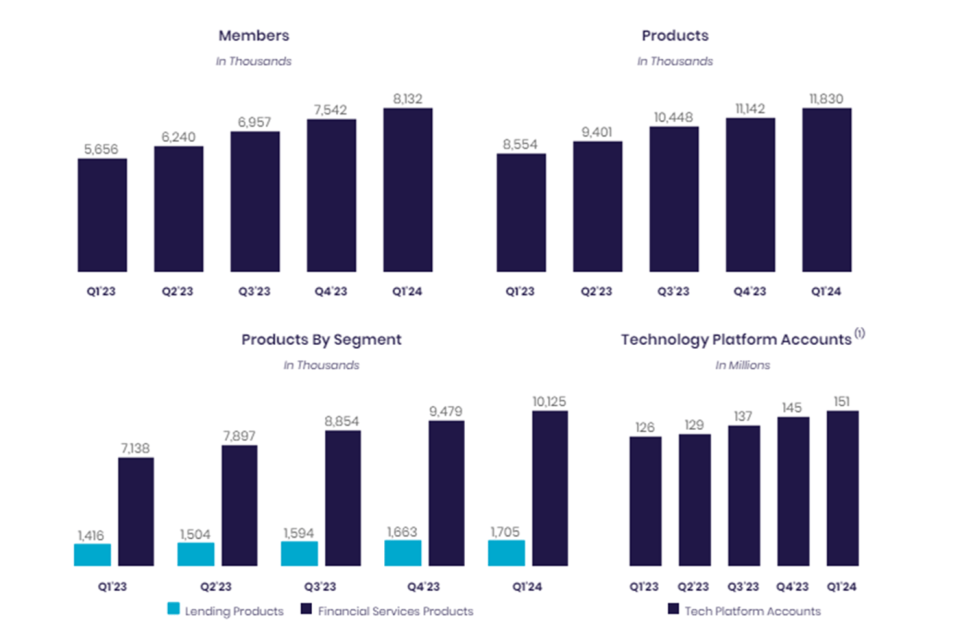

SoFi’s original business was in student loans, but it has since expanded into a full financial services provider. It’s popular with the students and young professionals that are its target market, and members have been increasing their engagement with its platform.

It acquired Golden Pacific Bancorp in 2022, obtaining a bank charter in the process, and it now offers bank accounts in addition to credit cards, investment tools, and other financial services. SoFi has been attracting new customers with its easy-to-use products, low fees, and high savings rates, and it has been successfully upselling and cross-selling new products to those established customers. This is what management calls its financial services productivity loop.

SoFi also has a technology platform segment that further diversifies its business. It offers fintech infrastructure for business clients through its Galileo and Technysis businesses, which it acquired in 2020 and 2022, respectively, and has stated a goal of becoming the Amazon Web Services of fintech. Combined revenues from the technology platform and financial services segments increased by 54% year over year in the first quarter.

So far, management’s strategy has produced incredible results. Members and product adoption are increasing at high rates, leading to strong revenue growth. Cross-selling generates growth without customer acquisition costs, and that has trickled down to the bottom line. Revenue increased 37% year over year in the first quarter, and it booked diluted earnings per share (EPS) of $0.02.

SoFi is expanding into new services, attracting millions of new customers, and growing its top and bottom lines at robust rates. So why is Wall Street so negative about its stock right now?

What about the lending business?

The numbers back up SoFi’s strategy, but Wall Street isn’t buying it (pun intended). SoFi’s core business is lending, and the lending business is under pressure. When a company’s core business isn’t functioning as well as Wall Street hopes, that creates doubt about its overall health.

The total number of loans SoFi has on its books is increasing, and that figure was up 20% year over year in the first quarter. Originations rose 22%. However, new revenue from its lending products declined by 2% year over year. Loan balances increased and its net interest margin expanded, driving a 33% increase in net interest income to $267 million. Non-interest income — which typically comes from things like service and transaction fees — declined by 53% to $64 million. Management is taking a cautious approach to loan approvals in this higher interest rate environment.

Wall Street may have focused on management’s forecast that 2024’s lending revenues would only be 92% to 95% of what they were in 2023. The company also guided for the other segments’ revenues to increase significantly, compensating for the weaker performance of the lending business. But these are the newer and less reliable segments, so overall, this was confidence-busting guidance.

Will SoFi stock bounce back?

The lending business may remain under pressure until interest rates go down, but SoFi’s ventures into other services are picking up the slack. SoFi reported its first quarterly net profit according to generally accepted accounting principles (GAAP) in the fourth quarter, and management expects to sustain that profitability through this year, and likely on an ongoing basis.

At current prices, this stock looks like an opportunity for forward-thinking investors. SoFi’s expansion efforts are working, and its lending business should rebound under improved conditions. No matter how it plays out, the broadening of its business is a positive step, and SoFi is on its way to becoming a financial industry powerhouse.

Should you invest $1,000 in SoFi Technologies right now?

Before you buy stock in SoFi Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SoFi Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $746,217!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Jennifer Saibil has positions in SoFi Technologies. The Motley Fool has positions in and recommends Amazon. The Motley Fool has a disclosure policy.

SoFi Stock Is Tanking: What Wall Street Is Getting Wrong was originally published by The Motley Fool

Signup bonus from