Nvidia (NASDAQ: NVDA) has benefited tremendously from the early phases of the artificial intelligence (AI) boom. Shares are up 800% since ChatGPT debuted in late 2022, and Nvidia recently achieved a $3 trillion market capitalization, surpassing Apple as the second-largest public company.

Nvidia executed a 10-for-1 stock split last Friday to bring its share price down to a more reasonable level, but Wall Street remains overwhelmingly bullish. Among the 62 analysts that follow Nvidia, 90% rate the stock a buy and 10% rate the stock a hold. No analysts recommend selling at the present time.

Additionally, Beth Kendig, lead tech analyst at the I/O Fund, recently told CNBC that Nvidia could be a $10 trillion company by 2030 due to the “impenetrable moat” arising from its superior hardware and popular CUDA software.

Interestingly, Mad Money host Jim Cramer made the same prediction back in 2021. For Nvidia to be a $10 trillion company by 2030, the stock would need to increase 233%, which equates to an annual return of 20% over the next six-and-a-half years.

Here’s what investors should know about Nvidia.

Nvidia has a durable advantage in its full-stack computing platform

Nvidia is the leading provider of data center graphics processing units (GPUs), chips used to speed up computationally complex workloads like artificial intelligence (AI) applications. The company accounted for 92% of data center GPU sales in 2023, according to IoT analytics.

Perhaps more importantly, Nvidia GPUs are the gold standard in AI infrastructure. The Wall Street Journal recently reported that “Nvidia’s chips underpin all of the most advanced AI systems, giving the company a market share estimated at more than 80%.” Indeed, some analysts estimate its market share at 95%.

What truly makes Nvidia formidable is its full-stack strategy encompassing hardware, software, and services. Beyond GPUs, Nvidia provides networking hardware and central processing units (CPUs) purpose-built for AI, as well as subscription software and cloud services that support AI workflows.

One particularly important element of that full-stack strategy is CUDA, a programming model that lets GPUs (originally designed for graphics workloads) accelerate any computing task. CUDA cements Nvidia’s leadership in data center use cases like AI because (1) it only runs on Nvidia chips and (2) no other company offers a comparable software ecosystem for developers.

Today, CUDA encompasses more than 250 software libraries (application building blocks), and it supports newer products like Nvidia AI Enterprise, a software platform that streamlines AI application development and deployment across a use cases like recommender systems, conversational assistants, logistics robots, and autonomous vehicles.

Nvidia benefited from strong demand for AI products in the first quarter

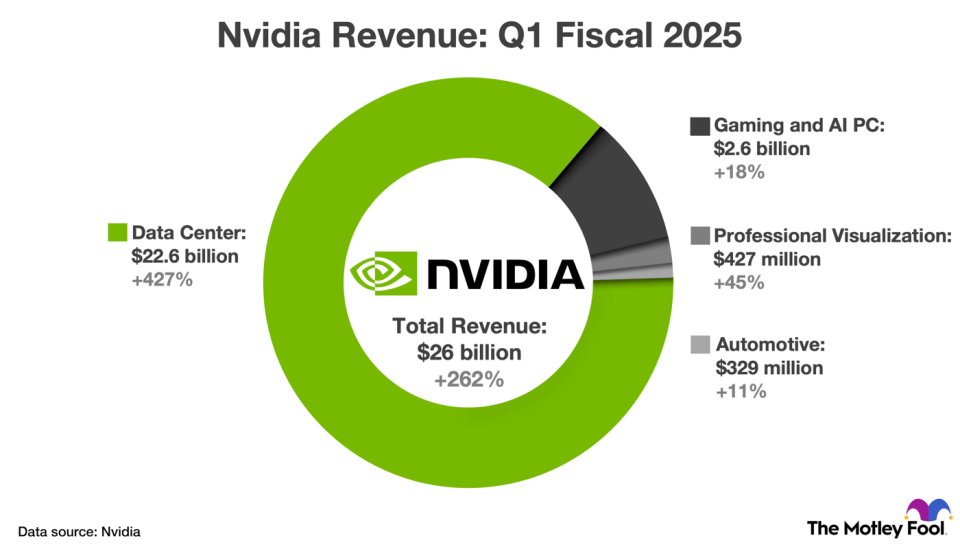

Nvidia reported phenomenal financial results in the first quarter of fiscal 2025 (ended April 28). Revenue rose 262% to $26 billion on strong sales growth in the data center segment driven by unprecedented demand for AI solutions. Meanwhile, non-GAAP net income increased 461% to $6.12 per diluted share.

The chart below provides detail on Nvidia’s first-quarter revenue growth across its primary product categories.

Looking ahead, CFO Colette Kress says “demand may exceed supply well into next year” due to the upcoming launch of Blackwell GPUs, the next generation of Nvidia’s AI platform. Blackwell GPUs delivers up to four times faster AI training and 30 times faster AI inferencing as compared to the previous Hopper architecture.

Nvidia stock is somewhat pricey, but not unreasonably expensive

The graphics processor market is forecasted to compound at 28% annually through 2030, and AI spending across hardware, software, and services is projected to grow at 37% annually during the same period. That gives Nvidia a good shot at annual earnings growth around 30% through the end of the decade.

Indeed, Wall Street expects the company to grow earnings per share at 31.8% annually over the next three to five years. That estimate makes its current valuation of 71.5 times earnings seem a little pricey, but not unreasonably so. In that context, it is possible for Nvidia to be a $10 trillion company by the end of the decade.

Specifically, if earnings grow at 30% annually through 2030, Nvidia’s market capitalization would reach $10 trillion if shares traded at roughly 40 times earnings. That would be a discount to the current multiple, but still an expensive valuation compared to the S&P 500 average of 24.7 times earnings.

Personally, I do not think investors should count on that outcome — a lot would have to go right for Nvidia over the next six-and-a-half years — but I do think patient, risk-tolerant investors should own a small position in Nvidia.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $746,217!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 10, 2024

Trevor Jennewine has positions in Nvidia. The Motley Fool has positions in and recommends Apple and Nvidia. The Motley Fool has a disclosure policy.

This Stock-Split Artificial Intelligence (AI) Stock Could Be a $10 Trillion Company by 2030, According to a Wall Street Analyst was originally published by The Motley Fool

Signup bonus from