For over 50 years, restaurant chain Cracker Barrel Old Country Store (NASDAQ: CBRL) has been pleasing customers with Southern style comfort food, old-timey products in its country store, and unique antique decor throughout its locations. Weary interstate travelers stop in, relax in some front-porch rocking chairs, and perhaps even play a game of checkers.

This nostalgic recipe has propelled Cracker Barrel into a well-known chain of 660 locations. But unfortunately for investors, it’s worth just a small fraction of some younger, thriving restaurant chains.

The Mediterranean-themed restaurant chain Cava Group (NYSE: CAVA) is a good example. As of April 21, Cava had only 323 locations — about half the footprint of Cracker Barrel.

Moreover, Cava was only just founded in 2010. In other words, Cracker Barrel had a head start of four decades to create shareholder value. But Cava is already out in front by a country mile.

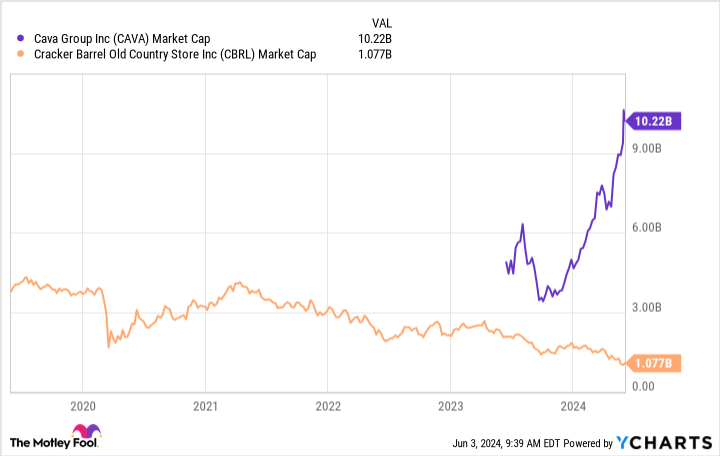

For evidence, we can compare the market capitalizations of both restaurant chains — the value of the companies based on current stock market prices. Cava’s market capitalization is up over $10 billion, whereas Cracker Barrel’s has sunk down to a measly $1 billion. Therefore, Cava is worth 10 Cracker Barrels, in a manner of speaking.

Here are some thoughts on the valuation disparity between Cracker Barrel and Cava. And, more importantly, here are some thoughts on what to do about it.

Why is Cava worth so much more?

Up front, understand that these business models are the same: Cracker Barrel and Cava don’t franchise their restaurants — they’re all company-owned. There is a small difference in how the two companies go about it: Cava leases the real estate for all of its locations, whereas Cracker Barrel owns the real estate for about half of its restaurants.

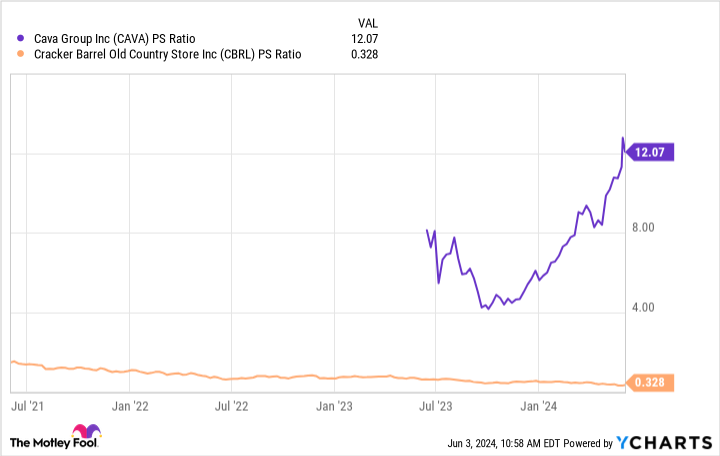

That’s not the difference maker for these two companies. The biggest differentiator is the valuation for the stocks. Looking at it from a price-to-sales (P/S) valuation, Cava stock is about 37 times more expensive than Cracker Barrel stock.

Why are investors willing to pay such a higher valuation for Cava? To put it simply, Cava is executing far better than Cracker Barrel.

One of the most glaring differences in operations has to do with labor expenses. Cracker Barrel has already reported financial results for the first three quarters of its fiscal 2024. During this time, 36% of the company’s revenue went to pay its workers. By comparison, Cava spent just under 26% of its revenue on labor — that’s a huge difference.

This is just one example of Cava’s superior operations. As a result, the company’s restaurant-level profit margins are around 25%. Cracker Barrel has an overall operating margin of less than 3%, which is down significantly from its margin of over 10% in 2017 — it’s been a steady, multi-year decline.

Lastly, investors are willing to pay up for Cava stock because it’s much higher growth. Not only are same-store sales increasing at a nice pace, but management is also opening up new locations — 14 in the most recent quarter alone.

Should investors buy the cheaper stock?

Buying cheap stocks is a relentless temptation for some of us. It feels safer. After all, if something is already cheap, it doesn’t seem reasonable that it would get even cheaper.

Moreover, the upside always seems compelling. Take Cracker Barrel for example: As shown above, it trades at a P/S multiple of 0.3. The stock could triple in value and still have a reasonable price tag.

However, investors should ask why Cracker Barrel stock could suddenly get a better valuation. In my opinion, the business would first need to tangibly improve for this to happen. Then investors might bid the valuation higher out of excitement.

In short, those who buy a cheap Cracker Barrel stock are betting on a turnaround — and in fairness, the company has ideas. For example, CEO Julie Masino recently pointed out that it’s cutting certain menu items and eliminating unnecessary labor-intensive food preparation processes. That could help.

But in my investing career, I’ve observed more failed turnarounds than I could shake a stick at. Cracker Barrel doesn’t have a straightforward path, and it will likely take time.

By contrast, companies with strong execution are usually hard to derail. I’d be hesitant to buy Cava stock today at its rich P/S of 12 — I’ve rarely seen a restaurant stock so expensive. That said, the company has some of the strongest financials that I’ve seen in the space, and I’d be willing to bet that these stay strong for the long haul.

I’m not necessarily saying that valuation doesn’t matter or to run out to buy Cava stock today. But counterintuitively, it can be safer to buy an expensive stock with a strong business, rather than buying a cheap stock in hopes of a turnaround. Over long time horizons, poor businesses keep eroding shareholder value, while strong businesses create it.

Should you invest $1,000 in Cava Group right now?

Before you buy stock in Cava Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Cava Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $713,416!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 3, 2024

Jon Quast has no position in any of the stocks mentioned. The Motley Fool recommends Cava Group and Cracker Barrel Old Country Store. The Motley Fool has a disclosure policy.

Don’t Look Now, but Cava Is Worth 10 Cracker Barrels. Time to Buy the Stock? was originally published by The Motley Fool

Signup bonus from