Energy Transfer (NYSE: ET) continued to build its pipeline and midstream empire when it recently announced the acquisition of WTG Midstream. At a price tag of around $3.25 billion, this is not a transformational deal by any stretch for a company with an over $52 billion market capitalization.

However, it is a good example of what the company does well and why investors should continue to be excited for the stock.

Empire building

In the past, institutional investors have criticized Energy Transfer for being more concerned about empire building than unitholder returns. In some ways this criticism is fair, but in other ways it is not.

Energy Transfer got a bit ahead of itself building its midstream empire and did have to cut its distribution in half during the pandemic to help reduce debt and lower leverage. However, it also did quickly get itself back into a good financial situation and has since increased its distribution to above where it was before the cut.

That said, I find Energy Transfer not always listening to its critics to be a good thing, because management is playing the long game, while many institutional investors are not in the stock for the long haul. Energy Transfer has a long history of buying assets and making them more valuable as a part of its integrated system.

Some examples include the company’s acquisition of Semgroup in late 2019 for its underutilized Houston Fuel Oil Terminal. The company then built a crude pipeline link to the terminal, which gave it the ability to transport crude out of the Houston market to other locations. Then in 2021, it bought Enable, converting some pipelines to different products and connecting it to its system to be able to give customers access to premium priced markets.

Last year, it acquired Lotus Midstream and Crestwood Equity Partners, which owned one of the largest gathering systems in the Bakken that it could then tie to its long-haul Dakota Access Pipeline.

The Crestwood and Lotus acquisitions also expanded Energy Transfer’s assets in the Permian, which is also what its WTG acquisition will do. With the WTG deal, Energy Transfer will add more than 6,000 miles of natural gathering pipelines and eight processing plants in the Permian, along with two facilities under construction. It also will will obtain a 20% interest in the BANGL NGL Pipeline, although its other owners will have the right to acquire the asset first.

Energy Transfer is paying $2.45 billion in cash and approximately 50.8 million units in the deal. It expects it to be immediately accretive to its distributable cash flow (DCF) per unit by $0.04 next year, rising to $0.07 by 2027.

The company said the deal will give it access to growing supplies of natural gas and NGL (natural gas liquids) volumes that will help improve its overall Permian operations. With the Permian still the premier oil basin in the U.S., continuing to obtain midstream assets in the basin to build out its system in the area is a smart long-term move. The company has restored its balance sheet to make this a largely cash deal and make it immediately accretive and growth to its DCF on a per-unit basis.

However, the most important thing with the deal is that it continues to add to the company’s scale in the Permian and could complement and feed into its proposed Warrior Pipeline, which it has said would give it “access to almost every major city gate in the state of Texas.”

A great value

Through growth projects and acquisitions, Energy Transfer has created one of the most impressive integrated midstream systems in the U.S. And while some have criticized its empire building and would prefer it take actions like buy back its undervalued stock, the company makes no apologies for its strategy and long-term goals.

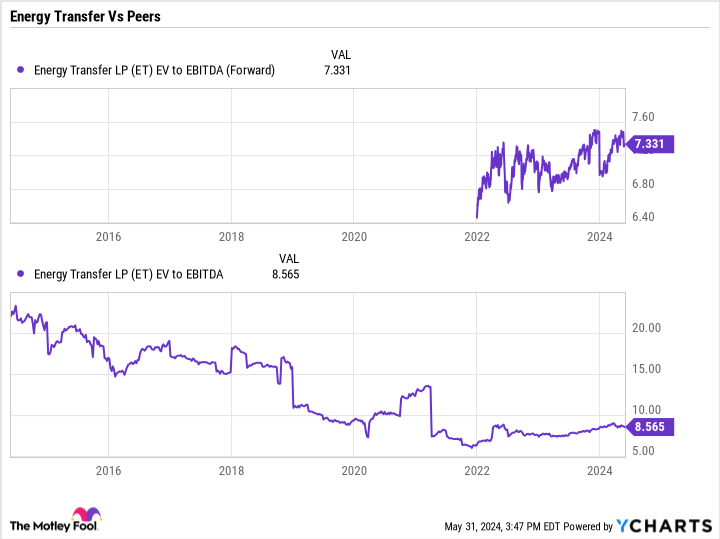

Trading at 7.3 times on an enterprise value (EV)-to-forward EBITDA basis, the stock is cheap compared to where it generally traded before the pandemic, although it is a much more financially healthy company with a better balance sheet and generating excess cash flow after growth capital expenditures and distribution payouts.

The master limited partnership (MLP) carries with it a robust 8.2% yield based on its most recent quarter distribution, with a goal of increasing it by 3% to 5% a year moving forward. As such, the stock looks like an attractive investment given its valuation, well-covered distribution, and growth outlook.

Energy Transfer may be building a pipeline empire, but that’s a good thing for long-term investors, as long as it continues to do so in its current prudent manner.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $713,416!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 3, 2024

Geoffrey Seiler has positions in Energy Transfer. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Energy Transfer Adds to Its Pipeline Empire With Another Acquisition. Why That Is a Good Thing for This 8.2% Yielding Stock. was originally published by The Motley Fool

Signup bonus from