The stock market has gotten off to a roaring start in 2024. Both the S&P 500 and Nasdaq Composite are trading at record levels, and the momentum doesn’t appear to be slowing down.

One of the big contributors to market gains this year is big tech. Indeed, the “Magnificent Seven” stocks have become synonymous with all things related to artificial intelligence (AI).

Among this cohort of megacap tech, Nvidia (NASDAQ: NVDA) might be the most closely followed — and for good reason. The company’s graphics processing units (GPUs) and data center services are acting as the main engine for an ever-evolving list of generative AI applications across all industry sectors.

Since going public in 1999, Nvidia stock has generated a total return of 138,700%. This means that if you’d invested just $1,000 on the day of the initial public offering (IPO) and held until today, your position would currently be worth approximately $1.4 million.

While it might seem like it’s too late to ride the Nvidia train, one Wall Street analyst thinks there’s more upside. C.J. Muse of Cantor Fitzgerald recently upgraded his price target for Nvidia to $1,400 — implying roughly 34% upside from current trading levels.

Let’s dig into Nvidia’s business, and assess why the company’s best days look like they are ahead.

Nvidia’s business is firing on all cylinders

Nvidia is the brains behind an impressive roster of GPUs. Its semiconductor chips are used for training large language models and a host of machine learning applications. Currently, Nvidia’s A100, H100, and Blackwell chips are considered to be the best GPUs available.

The demand for Nvidia’s GPUs can be summed up in just one statistic: The company currently owns an estimated 80% of the addressable market for AI-powered chips.

Given its dominant position in the chip market, Nvidia is able to command strong pricing power. This is an important dynamic to understand, because it directly impacts Nvidia’s entire business.

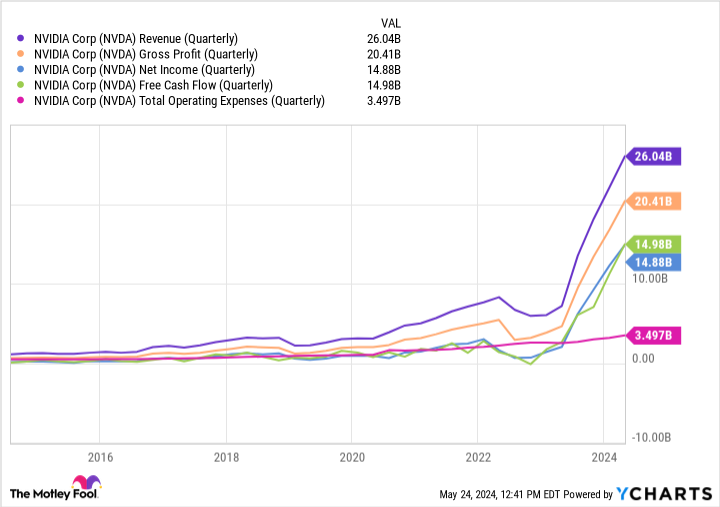

From the chart above, you might notice that Nvidia’s operating expenses have started to rise significantly over the last couple of years. While strong demand for its products and services is a good thing, matching supply output can be a costly endeavor.

Generally, when businesses experience hiccups in the supply chain or are choosing to invest hefty sums into research and development to innovate at a faster pace over the competition, operating margins and profitability can take a hit.

However, this is not the case with Nvidia. The company is in a unique position in that demand for its services is so high, that Nvidia can raise its prices and customers will still pay them. So, despite a rising expense profile, Nvidia is actually increasing its revenue at a faster pace.

This dynamic is especially lucrative considering that Nvidia’s gross profit margin is expanding, which is dropping straight to the bottom line.

During the company’s first quarter of 2024, revenue accelerated 262% year over year while free cash flow grew by nearly sixfold to $14.9 billion.

Where is Nvidia stock headed?

It’s understandable if you’re wary about Nvidia’s ability to keep up this growth pace. Considering competitors such as Advanced Micro Devices and Intel already offer competing chips, and big tech stalwarts such as Amazon and Meta Platforms are developing their own lines of chips internally, I’d say it’s more than likely that Nvidia will eventually begin to lose market share.

With that said, I see rising competition as a positive. Keep in mind, Nvidia’s original mission 20 years ago was to develop technology to enhance the graphics in video games. While gaming is still an important pillar of Nvidia’s business, the company has done a stellar job branching into other areas of computing. Moreover, the decision to pursue avenues outside of gaming have proved worthwhile, as Nvidia’s largest businesses now stem from AI-related services.

I can’t say for certain if and when Nvidia stock will rise to $1,400 per share. However, I’m incredibly bullish that even better days are ahead. For now, the company is the bona fide leader in AI chips, and the company’s soaring profits provide Nvidia with unparalleled financial flexibility that it can use to explore further sources of growth.

Considering the AI revolution is very much in its early chapters, Nvidia should continue benefiting from secular tailwinds for years to come. Investors with a long-term horizon might want to consider scooping up shares of Nvidia right now. The company has already minted many millionaires, and the current growth trajectory suggests that a new wave has arrived.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $703,539!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 28, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Amazon, Meta Platforms, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, Meta Platforms, and Nvidia. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel and short May 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

This Stock Turned $1,000 Into $1.4 Million, and 1 Wall Street Analyst Thinks It Could Soar Another 34% was originally published by The Motley Fool

Signup bonus from