One of the stocks I’ve held longest in my portfolio is pipeline company Enterprise Products Partners (NYSE: EPD), which I’ve owned for over 15 years. Despite having owned it for so long, I’m just as excited to own it today as I was when I first bought the stock.

Let’s look at five reasons why I suggest buying the stock like there is no tomorrow.

1. Consistency

Enterprise has been one of the most consistent companies over the past two decades. This stems from owning a large integrated midstream system that is diverse in geography, product, and market. The company has over 50,000 miles of pipelines that is uses to transport various hydrocarbons, such as natural gas, crude oil, and natural gas liquids (NGLs), as well as over 300 million barrels of liquid storage. It also owns processing plants, fractionators, petrochemical facilities, and deepwater docks.

Enterprise’s assets touch most of the midstream value chain. This helps create a natural hedge for the company, as it can direct, store, and upgrade products in order to create the most value for customers and itself.

In addition, typically 80% or more of the company’s business is fee-based, so it has modest commodity and spread exposure. In addition, about half of its fee-based revenue comes from long-term take-or-pay customers, which means it gets paid whether its pipelines and assets are being used or not.

Enterprise’s business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [capex]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016.

2. High yield and growing distribution

Enterprise’s consistency has allowed it to raise its distribution for 25 consecutive years. This includes through such difficult periods as the financial crisis, the oil price collapse, and the early days of the pandemic.

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage, which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. (The company defines leverage as net debt adjusted for equity credit in junior subordinated notes divided by adjusted EBITDA.)

Enterprise currently has a robust forward yield of 7.2% based on its $0.515 quarterly distribution. With a 1.7 coverage ratio over the past 12 months and low leverage, the distribution is well covered and set to continue to rise in the coming years, extending Enterprise’s current streak.

3. Growth opportunities

Enterprise is also set to ramp up growth after it decided to slow projects down during the early days of the COVID pandemic given uncertainty at the time. The pipeline company brought its organic growth capex up to $2.9 billion last year and it currently plans to spend around $3.5 billion on growth projects both this year and next.

Projects take time to build and then ramp up, so the impact of these projects should start to be felt later this year and beyond. The company typically has gotten a 13% return on invested capital over the past several years. This means that for every $1 billion it spends on growth capex, it would generate $130 million in incremental annual gross operating profit.

Meanwhile, Enterprise also just recently announced that after five years it has finally received an important deepwater port license needed for its proposed Sea Port Oil Terminal (SPOT) project. If the project is built, it will turn Enterprise into an important player in crude exports.

Overall, the company is set to reenter growth mode at a time when it has excess cash to spend.

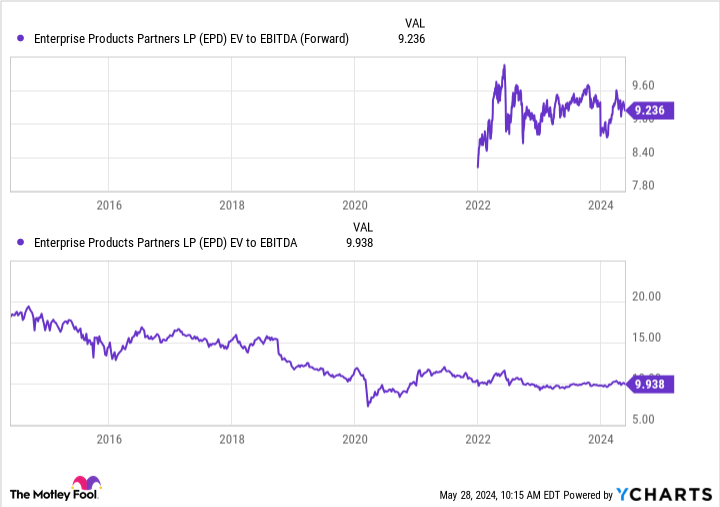

4. Inexpensive valuation

Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3 forward enterprise value (EV)-to-EBITDA multiple. This is one of the most common ways to value midstream stocks, as it takes into account their net debt while taking out non-cash expenses.

This is much lower than the over 15 multiple that Enterprise often traded at before the pandemic. It’s also well below the 13.7 multiple the average midstream master limited partnership (MLP) traded at between 2011 and 2016, when it had higher leverage and less attractive business models.

5. Deferred taxes on distributions

Enterprise has a long history of being a consistent performer operationally and has strong growth projects ahead. In addition, it has a high yield, growing distribution, and an inexpensive valuation by historical standards.

What could make an investment in the stock even more attractive? How about tax-deferred distributions.

That’s right. As an MLP, Enterprise technically pays out a distribution that is largely considered a return of capital, and not a dividend. The return of capital portion of the distribution is tax deferred and lowers the owner’s cost basis and thus isn’t taxed until the stock is sold.

Now this benefit does come with investors being issued a K-1 tax form at tax time. However, this extra form is just a minor inconvenience and can generally be easily handled by an accountant or tax program. The tax-deferred distributions are well worth the extra paperwork.

Should you invest $1,000 in Enterprise Products Partners right now?

Before you buy stock in Enterprise Products Partners, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Enterprise Products Partners wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $697,878!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 28, 2024

Geoffrey Seiler has positions in Enterprise Products Partners. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

5 Reasons to Buy Enterprise Products Partners Stock Like There’s No Tomorrow was originally published by The Motley Fool

Signup bonus from