Energy Transfer (NYSE: ET) continues to lead the midstream sector’s consolidation. The master limited partnership (MLP) made two deals last year and recently followed them up with its first acquisition in 2024. It’s paying nearly $3.3 billion to buy WTG Midstream.

Its latest deal perfectly aligns with its acquisition strategy of finding accretive transactions that enhance its value chain without negatively impacting its balance sheet. That approach should continue paying dividends for investors by giving the MLP the fuel to keep growing its high-yielding distribution (currently over 8%).

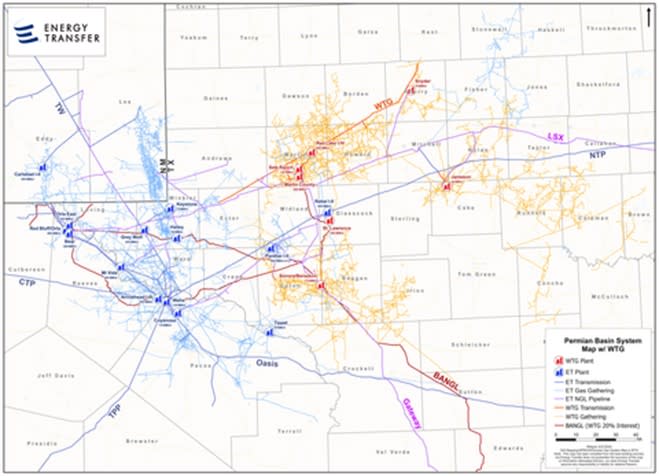

Drilling down into Energy Transfer’s latest deal

Energy Transfer is buying WTG Midstream for roughly $2.5 billion in cash and 50.8 million units (nearly $3.3 billion). That deal structure positions Energy Transfer to earn strong equity returns while maintaining its targeted leverage ratio. The company expects the highly accretive deal will boost its distributable cash flow per unit by $0.04 per share in 2025, increasing to $0.07 per unit by 2027.

WTG Midstream fits Energy Transfer like a glove. It will enhance and expand the company’s gathering and processing position in the Permian Basin. WTG Midstream owns 6,000 miles of gas-gathering pipelines in the Midland Basin side of the Permian. It has eight operating natural gas processing plants with capacity of 1.3 billion cubic feet per day (Bcf/d). It also has a 20% ownership interest in the BANGL natural gas liquids (NGL) pipeline. Long-term contracts with high-quality customers back these highly complementary assets:

Energy Transfer expects to close the transaction in the third quarter. It will supply the MLP with incremental income that should grow over the next few years as the company completes some associated expansion projects and captures commercial and cost synergies.

Built-in growth

WTG Midstream will increasingly add incremental revenue for Energy Transfer over the next several years. The acquisition will supply the MLP with highly visible near-term growth as it completes expansion projects currently under construction. It will also feed NGLs to its downstream assets, boosting their volumes and fees.

WTG Midstream is building two more natural gas processing plants that will add 0.4 Bcf/d of additional capacity. The company expects the first plant to come online in the third quarter and the second in the third quarter of 2025. In addition, the joint venture partners who own the BANGL pipeline are expanding the 125,000 barrel-per-day pipeline (BPD) to 200,000 BPD. That expansion should enter service in the first half of next year. The partners could ultimately expand that pipeline to over 300,000 BPD.

Energy Transfer expects the acquisition to unlock new expansion opportunities in the future. As producers in the Midland Basin grow their production, Energy Transfer can build additional gathering pipelines and processing plants. Meanwhile, the increasing upstream volumes could eventually drive expansions downstream, including additional pipeline expansions, new NGL fractionation capacity, and more export capacity. These factors power the company’s view that the transaction will grow its distributable cash flow per share over the next several years.

That growing cash flow will help support Energy Transfer’s plans to increase its distribution. The MLP aims to raise its payout by $0.0025 per unit each quarter ($0.01 annually), implying that this deal alone could fuel its distribution growth for several years. It could allow the company to accelerate its distribution growth rate toward the higher end of its 3% to 5% annual target range (it delivered a 3.3% increase over the past year).

Another smart deal

Energy Transfer continues to find highly accretive acquisitions that enhance its value chain. This strategy enables the MLP to grow its cash flow per share, giving it more fuel to increase its big-time payout. The WTG Midstream deal alone could fuel distribution growth for several years, making the MLP an even more attractive option for income-seeking investors.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 28, 2024

Matt DiLallo has positions in Energy Transfer. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Energy Transfer Continues Its Acquisition Binge With This $3.3 Billion Deal (Giving It a Lot More Fuel to Increase Its High-Yielding Payout) was originally published by The Motley Fool

Signup bonus from