Data cloud company Snowflake (NYSE: SNOW), a Wall Street favorite, plunged nearly 20% following its fourth-quarter earnings for its fiscal year 2024. While the numbers played a role in the slide, CEO Frank Slootman announced his immediate resignation, which shocked Wall Street.

Snowflake immediately named Sridhar Ramaswamy as the new CEO, an internal promotion for the former head of artificial intelligence. Slootman will remain chairman of Snowflake’s board.

Investors are left to put the pieces together. However, this momentary stumble could be a great long-term buying opportunity.

I’ll detail why below.

Examining Snowflake’s leadership change

It can be unnerving whenever a company changes leadership, especially in the CEO position. The CEO of a company is like a ship’s captain. They set the tone for the business, including culture and strategic direction, and answer to shareholders about how it performs. But it’s crucial to understand some context around Slootman’s departure.

For starters, Slootman is 65 years old today. He was never the long-term answer at CEO. Based on his long-standing corporate career, he took the reins at Snowflake in 2019 to help the company make the transition from the private to the public market. He isn’t a company founder. He’s what I call an “operator.”

His job was likely to make sure the company was performing well during Snowflake’s first few years on Wall Street, making sure the business didn’t buckle under the scrutiny public companies receive. Slootman seemingly did his job well. Snowflake has beaten analysts’ revenue estimates every quarter as a public company.

Today, Snowflake is striving to become an important player in AI. The company has partnered with Nvidia to help customers use its data cloud platform to develop and deploy generative AI. Appointing Ramaswamy, who had already led AI within Snowflake, is a logical transition.

Ramaswamy will have to prove Snowflake can keep performing at a high level under his guidance, but everything behind the change makes sense.

Snowflake looks like it is underpromising

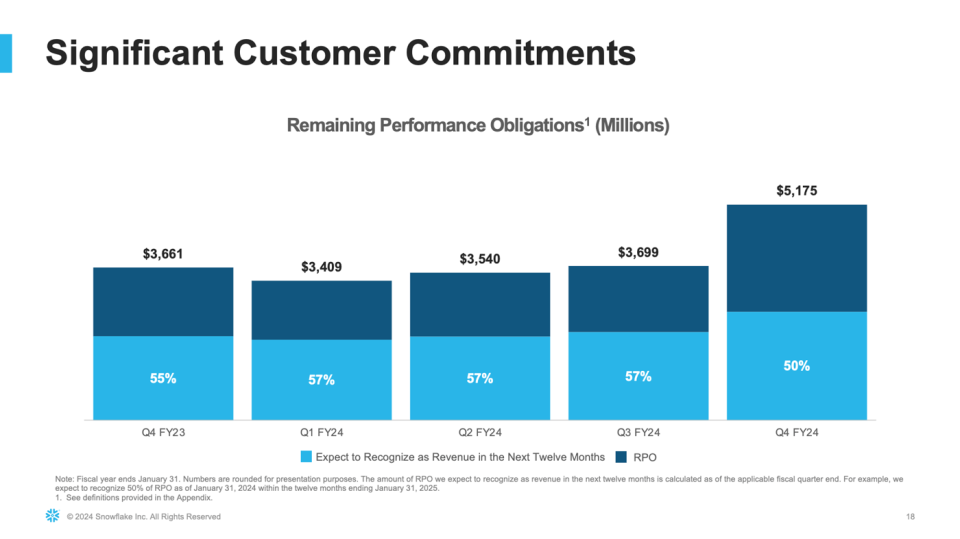

One could argue that soft guidance is a big reason Snowflake dropped after earnings. Management calls for 22% year-over-year revenue growth in fiscal year 2025, a slowdown from the 38% growth it just posted in fiscal year 2024. However, the evidence suggests Snowflake set a low bar the company might easily hurdle throughout the year.

Snowflake’s remaining performance obligations scream underpromise, over-deliver:

Snowflake saw a significant uptick in bookings this past quarter and expects to realize 50% of that, or just over $2.5 billion, as revenue over the next four quarters. The company just did $2.66 billion in revenue this past year. In other words, Snowflake is already set to eclipse last year’s revenue figure. Anything booked and billed over the next 12 months will be incremental growth.

Of course, investors will have to see what future quarters bring, but it seems likely that actual numbers will exceed guidance.

Shares just became more reasonably priced

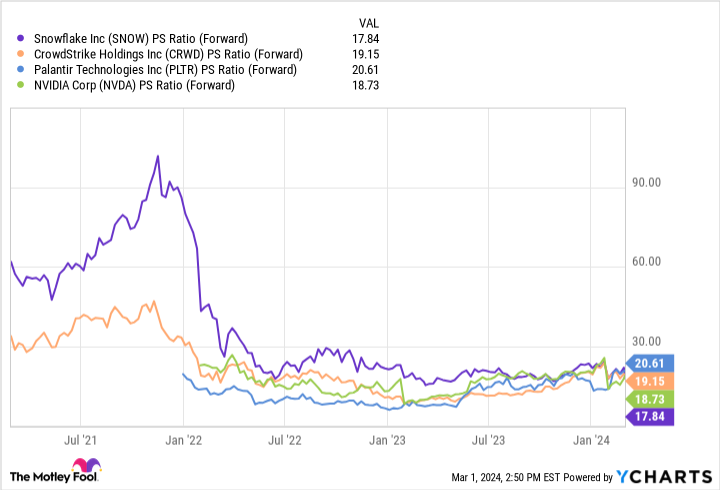

Snowflake went public during a bubbly stock market, so investors shouldn’t expect valuations to approach what they once were. However, you can see below that Snowflake continues getting less expensive. Now, at under 18 times revenue, the stock is valued like other highly regarded tech stocks across Wall Street, like Nvidia, Palantir, and CrowdStrike:

The dip makes Snowflake a stock that long-term investors can argue for buying, especially if using a dollar-cost averaging strategy to build their position slowly. Shares could remain volatile while Wall Street grapples with Snowflake’s recent changes, and the broader market has been notably jubilant in recent weeks.

But if Snowflake does end up thrashing its guidance, investors could be glad they bought the stock during this momentary uncertainty.

Should you invest $1,000 in Snowflake right now?

Before you buy stock in Snowflake, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Snowflake wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 26, 2024

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CrowdStrike, Nvidia, Palantir Technologies, and Snowflake. The Motley Fool has a disclosure policy.

Is Snowflake a Buy After the CEO Abruptly Stepped Down? was originally published by The Motley Fool

Signup bonus from