With shares up a whopping 244% year to date, Nvidia (NASDAQ: NVDA) stock has been a slam dunk for its near-term investors as the artificial intelligence (AI) boom sends demand for its data center chips through the roof. But what will the future bring — especially as more companies join this red-hot industry? Let’s dig deeper to find out how this technology giant may perform over the coming three years.

Why Nvidia?

If generative AI can be likened to the California Gold Rush, Nvidia is selling the picks and shovels via its advanced graphics processing units (GPUs). This hardware is crucial for training and running generative AI applications and giving data centers the computing power they need to offer AI-related solutions to their enterprise clients. The surging demand for these products shows no signs of stopping.

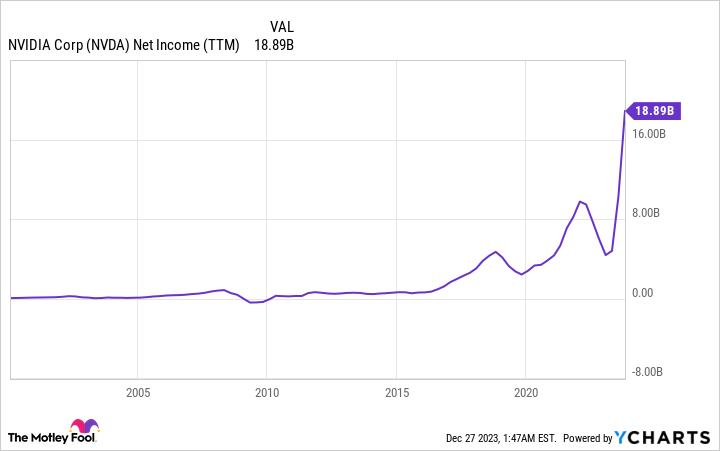

According to TechCrunch, Nvidia’s third-quarter revenue jumped 206% year over year to $18.1 billion based on sales of some of its highest-margin products, like the H100 data center chip, which can cost over $30,000. And with consumer demand shifting from Nvidia’s cheaper consumer GPUs to its most expensive offerings, the chipmaker could quickly become one of the world’s most profitable companies. In the third quarter, its net income margin rose from 46% to 51% while profits jumped by 588% to $10 billion.

Keeping the competition at bay

As with any new technology, the prospects of soaring growth and high margins are attracting more competition. For Nvidia, this will take two forms. First will be the cloud service providers, like Amazon and Alphabet, which are developing homegrown AI chips. But this will mainly be for internal use. These companies will probably be unable to completely end their reliance on Nvidia because of its technical lead as a GPU specialist and how fast demand is growing.

Nvidia’s most credible threat may come from its old rival, Advanced Micro Devices (AMD), also a big player in the GPU industry. The company is releasing its MI300 family of AI chips it claims outperforms Nvidia’s H100 on metrics like training and inference (running generative AI applications).

However, AMD’s CEO, Lisa Su, believes the market for AI chips will expand from $45 billion to $400 billion by 2027. This leaves plenty of room for both companies to sell these products as fast as they can make them.

Shares remain relatively affordable

With a market cap of $1.22 trillion, Nvidia is already the world’s sixth-largest company, behind e-commerce giant Amazon. The tech giant’s epic scale means it will be harder to impress the market, which could discourage growth investors. That said, Nvidia’s valuation isn’t as high as it looks. While its price-to-sales (P/S) ratio of 27 is over 10 times the S&P 500 average, the metric doesn’t account for Nvidia’s explosive growth rate or sky-high margins.

The stock’s forward price-to-earnings (P/E) ratio (which looks at projected 12-month net income) may give a better understanding of Nvidia’s worth. With a forward P/E of 25, shares are cheaper than the market average of 26. The company could become undervalued over the next three years if its stock price doesn’t rise fast enough to match its explosive AI-driven expansion.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 18, 2023

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Will Ebiefung has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, and Nvidia. The Motley Fool has a disclosure policy.

Where Will Nvidia’s Soaring Stock Be in 3 Years? was originally published by The Motley Fool

Signup bonus from