Nvidia (NASDAQ: NVDA) has captivated Wall Street this year as its business has exploded alongside a boom in artificial intelligence (AI). The company’s years of dominance in graphics processing units (GPUs) perfectly positioned it to cash in on a spike in demand for AI chips. Meanwhile, its competitors have yet to catch up.

Excitement over AI has seen Nvidia’s stock reach record heights this year, a stark contrast from the 50% plunge its share price took in 2022 amid an economic downturn. The company is on a promising growth trajectory, with its stock an attractive option heading into the new year.

As a result, now is an excellent time to learn more about this tech giant and potentially invest. So, here are five things to know about Nvidia stock.

1. Reaching new heights thanks to AI

Over the last 12 months, Nvidia has quite possibly enjoyed its best year in business since its founding 30 years ago. Its stock has skyrocketed 226% since Jan. 1. Meanwhile, the company has delivered quarter after quarter of stellar earnings growth.

In the third quarter of 2024 (ending October 2023), Nvidia posted revenue growth of 206% year over year, with operating income up more than 1,600%. The meteoric rise was primarily a result of a 284% increase in data center revenue, representing a spike in AI GPU sales.

The company massively profited from AI this year, and the industry is showing no signs of slowing. According to Grand View Research, the AI market hit a value of $137 billion in 2022 and is projected to expand at a compound annual rate of 37% until at least 2030. Nvidia has carved out a powerful role in AI and will likely continue profiting from the sector for years.

2. A lucrative role in video games

Nvidia is now a data-center-first company. But long before its expansion in markets like AI and cloud computing, the chipmaker’s highest earnings segment was gaming.

It was one of the first companies to begin selling GPUs to the consumer market, with the chips quickly becoming popular in the gaming community as gamers used Nvidia’s hardware to build powerful gaming PCs.

Besides its PC business, Nvidia is the primary chip supplier to Nintendo‘s Switch console. The portable gaming machine has sold more than 132 million units worldwide and is the third-best-selling console of all time (after Sony‘s PlayStation 2 and the Nintendo DS).

Like many markets across tech, the video games sector suffered from reductions in consumer spending last year. However, Nvidia posted an 81% year-over-year rise in gaming revenue in the 2024 third quarter, signaling a potential end to market declines.

3. AI chip competition will heat up in 2024

Increased interest in AI this year has led countless tech companies to pivot their businesses toward the high-growth industry. While most firms are focusing on the software side of the market, Nvidia’s meteoric rise has motivated many to venture into chip production, some for the first time.

While it’s not surprising that leading chipmakers like Advanced Micro Devices and Intel are gearing up to challenge Nvidia in AI, companies like Amazon and Microsoft have also announced expansions into hardware.

Many of these companies will launch their new chips in 2024 as they attempt to take a bite of Nvidia’s estimated 90% market share in AI chips.

For now, the biggest threat is likely AMD, which has been the second-biggest name in GPUs for years. AMD will launch what the company describes as its most powerful GPU ever in 2024, designed specially to go head-to-head with Nvidia’s offerings.

Nvidia’s dominance will be challenging to overcome, but prospective investors should be aware of increasing competition on the horizon.

4. Developing chips for China

Over the last year, the U.S. has introduced new restrictions on the export of high-powered chips to China alongside growing tensions between the two countries. The clampdown has made Nvidia investors slightly uneasy because sales to China make up about 20% of its data center revenue.

As in many countries worldwide, demand for AI computing power is soaring in China and represents a crucial growth market for Nvidia. As a result, the chipmaker is working closely with the U.S. to develop chips specifically for the Chinese market that will comply with export regulations and meet demand in the region.

It’s too soon to know how successful the China-specific chips will be, but it’s a situation worth keeping an eye on. The company is expanding quickly in other regions, which could offset at least a portion of potential lost sales, but only time will tell how much.

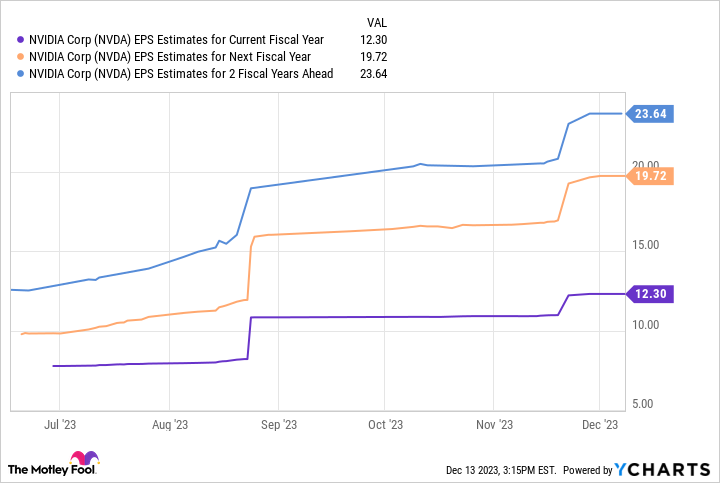

5. Stellar stock growth is projected over the next few years

This chart shows Nvidia’s earnings could rise close to $24 per share by fiscal 2026. Multiplying that figure by the company’s forward price-to-earnings ratio of 45 yields a stock price of $1,080, projecting growth of 125% from its current position over the next two years.

Nvidia has immense growth potential, with its stock an attractive buy right now and possibly too good to pass up.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 11, 2023

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Dani Cook has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Amazon, Microsoft, and Nvidia. The Motley Fool recommends Intel and Nintendo and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short February 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

5 Things to Know About Nvidia Stock was originally published by The Motley Fool

Signup bonus from